Today, a federal judge in Western Arkansas ruled that one of the fraud and racketeering cases against Gospel for Asia will go to trial in 2019. U.S. District Judge Timothy Brooks set the date for a jury trial on April 15, 2019.

Despite numerous legal maneuvers by GFA’s lawyers, the Murphy RICO case will move ahead. This is a significant win for the plaintiffs since GFA has tried on multiple occasions to have this and another case thrown out. The earlier case involving another Arkansas couple, Matthew and Jennifer Dickson, has been stayed pending an appeal by GFA.

Read the scheduling order here.

The 10 page order in Murphy and Murphy v. Gospel for Asia sets the dates for discovery throughout the remainder of this year and 2018:

1. TRIAL SET FOR APRIL 15, 2019

The trial of this matter is scheduled for a three to four week JURY TRIAL in FAYETTEVILLE, ARKANSAS, beginning on APRIL 15, 2019, at 9:00 a.m. The case will be tried to an nine (9) person jury–unanimous verdict required. Counsel are directed to report to the Fifth-floor Courtroom by no later than 8:30 a.m. on the first day of trial unless otherwise notified.

2. FINAL PRE-TRIAL CONFERENCE

A Final Pre-Trial Conference shall be conducted pursuant to the provisions of Rule 16(e) on APRIL 2, 2019, beginning at 9:00 a.m.

3. AMENDMENT OF PLEADINGS

Leave to amend pleadings and/or to add or substitute parties shall be sought no later than OCTOBER 19, 2017.

4. EXPERT DISCLOSURES

(a) Class Expert Witnesses Plaintiffs’ deadline to provide disclosures and written reports for class experts pursuant to Rule 26(a)(2) is OCTOBER 15, 2017. Defendants’ deadline to provide class expert witness disclosures and written reports pursuant to Rule 26(a)(2) is NOVEMBER 30, 2017. The deadline to provide disclosures and reports of rebuttal experts (i.e. whose testimony will be offered solely to contradict or rebut the expert opinions offered by an opposing class expert) is DECEMBER 15, 2017. (b) Merit Expert Witnesses Plaintiffs’ deadline to provide disclosures and written reports for merit experts pursuant to Rule 26(a)(2) is AUGUST 31, 2018. Defendants’ deadline to provide expert merit witness disclosures and written reports pursuant to Rule 26(a)(2) is OCTOBER 5, 2018. The deadline to provide disclosures and reports of rebuttal experts (i.e. whose testimony will be offered solely to contradict or rebut the expert opinions offered by an opposing merit expert) is OCTOBER 19, 2018.

5. DISCOVERY

The scope of discovery may include both class and merits discovery. That said, discovery which clearly has no purpose other than for merits issues should be deferred until after the Court rules on class certification. The discovery deadline is NOVEMBER 16, 2018. The parties may conduct discovery beyond this date if all parties are in agreement to do so. To avoid later misunderstandings, such agreements should be reduced to a writing which describes the type, scope, and length of the extended period of discovery. That said, the Court will not resolve any disputes which may arise in the course of extended discovery. All discovery requests must be propounded sufficiently in advance of the discovery deadline to allow for a timely response. Witnesses and exhibits not identified and produced in response to Rule 26(a)(1) Initial Disclosures, and/or in response to subsequent discovery requests, may not be used at trial except in extraordinary circumstances. The Court will not grant a continuance because a party does not have time in which to depose a lay or expert witness.

6. MOTIONS DEADLINES (a) Class Certification Motions: The deadline to file class certification motions is JANUARY 19, 2018. < Responses to class certification motions are due not later than six (6) weeks after the motion is filed. < Replies are due not later than three (3) weeks after the response is filed.

A settlement hearing was scheduled for January 31, 2019 in the event that the parties decide to settle.

ORDER SETTING SETTLEMENT CONFERENCE

This case has been referred to the undersigned for a settlement conference. All parties and their lead counsel are hereby ORDERED TO APPEAR before the undersigned at the U. S. Federal Building, 35 E. Mountain, Fayetteville, Arkansas, in Room 210 at 9:00 A.M. on January 31, 2019. All participating attorneys must be of record. An insured party shall appear by a representative of the insurer with the complete authority to agree to a settlement up to the policy limits. An uninsured corporate party shall appear by a representative authorized to agree to a settlement. If a public entity is a party, all of the members of the board of the public entity, or a quorum of the entity, who have complete authority to agree to a settlement–or a representative given such authority by the board members–shall appear. The complete authority to agree to a settlement means that the representative must have the authority to make an independent assessment of the value of the case and proposed settlement terms as the settlement discussions proceed. Each party shall, before arriving at the settlement conference, ascertain in good faith the best settlement proposal that such party can make and be prepared, if asked by the undersigned, to communicate that settlement proposal to the under-signed in confidence. If no settlement discussions have taken place, the court encourages an exchange of demands and offers prior to the settlement conference.

K.P. Yohannan and his co-defendants will need to be in attendance for this conference.

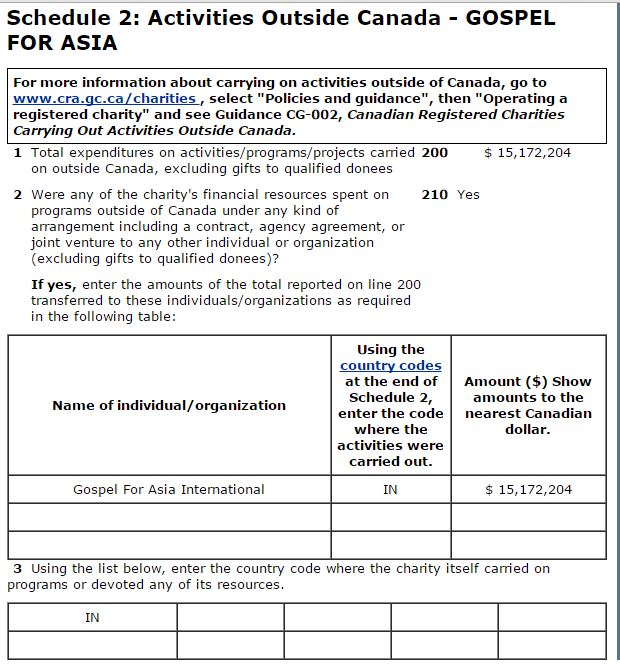

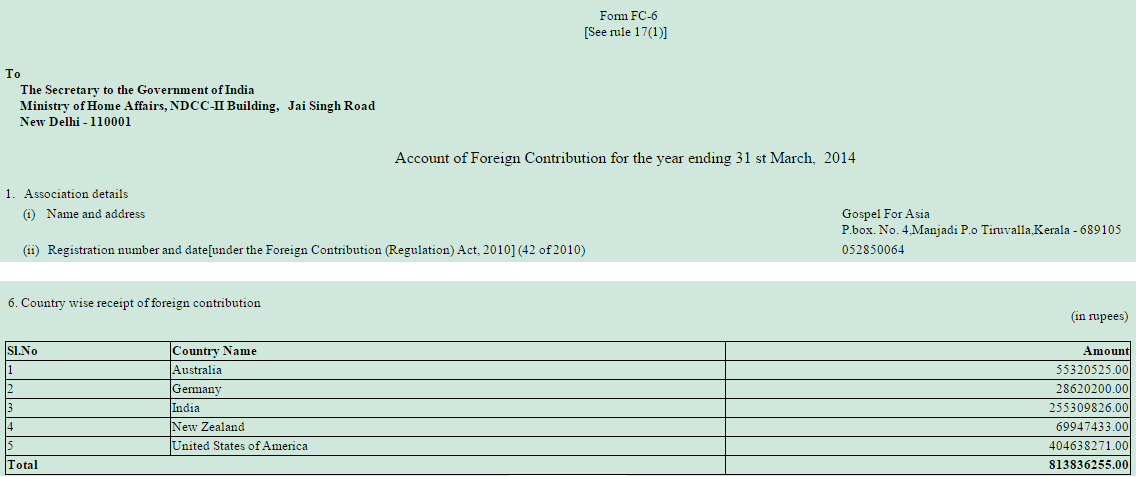

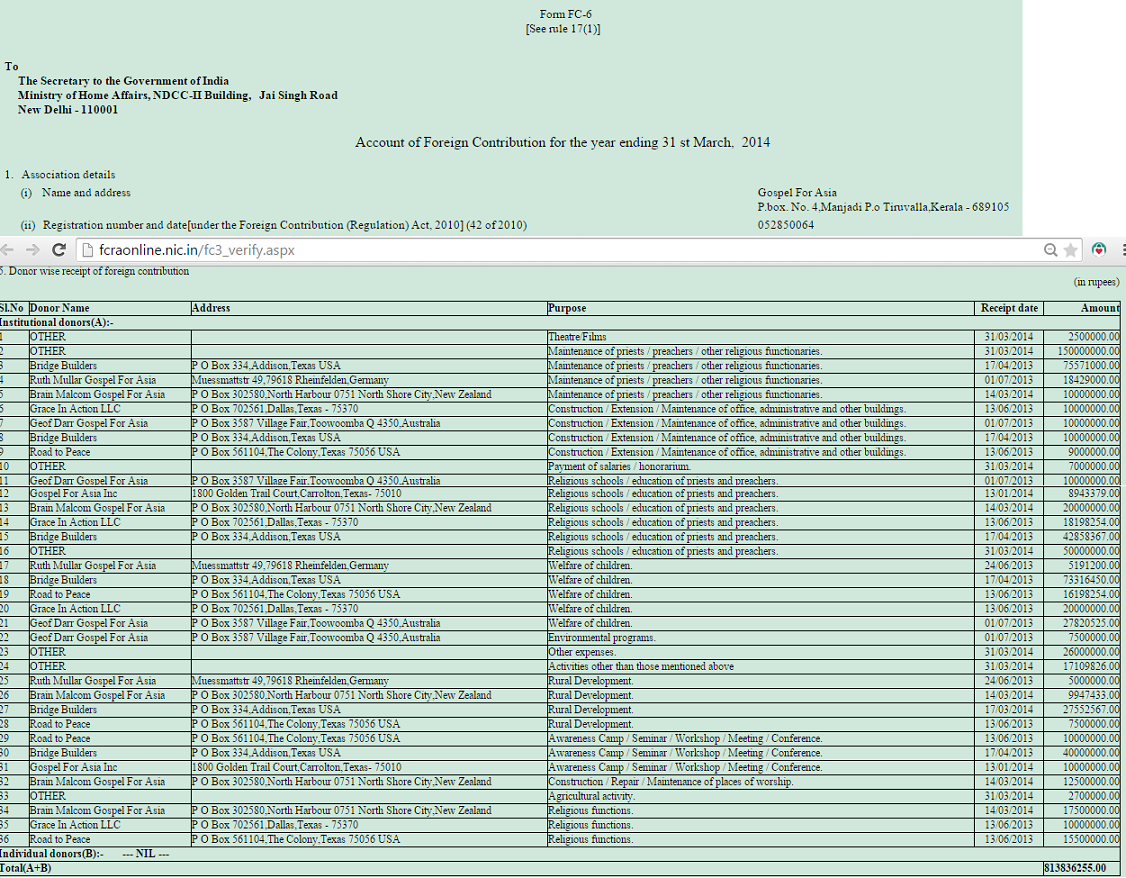

GFA must now submit to scrutiny that the organization has been resisting. GFA has not published an audited financial statement since FY 2013 and lost membership with the Evangelical Council for Financial Accountability in October, 2015.

I believe the GFA action is one of the largest evangelical charities to face a lawsuit of this kind.