On June 4, federal Judge Timothy Brooks sanctioned mission giant Gospel for Asia in the ongoing fraud case of Murphy v. Gospel for Asia for failure to produce evidence as requested multiple times by the court. The court found that GFA “needlessly squandered the resources of the parties…and put an ‘extraordinary drain on the Court’s resources,” and that GFA’s “abusive conduct in this case since August constitutes a willful violation of its discovery orders.”

In sanctioning GFA, Judge Brooks will require GFA to pay for a Special Master to oversee the gathering of evidence. In the process, this attorney will have the ability to appoint a forensic accountant and will have access to all pertinent GFA records and communications.

Setback for Gospel for Asia

This is a major setback for GFA. For several years, GFA has been defending itself by saying that all funds are spent as donors intend. However, now after months of telling Judge Brooks that this can be proven, GFA is no closer to producing the evidence.

In his order, Judge Brooks accuses GFA of evasive tactics and warns them that discovery is not a shell game. Furthermore, he denied GFA’s claims that they have no control over entities in India. He pointed to documents demonstrating wire transfers between entities, the fact that Yohannan’s family members sit on many boards in common, Yohannan’s prominent status in Believers’ Church and prior ability to get financial documents from organizations they say don’t control.

Judge Brooks had strong words for GFA saying that they had failed to “obey clearly worded directives issued by this Court and to respond in good faith to Plaintiff’s discovery requests.” The federal judge has found GFA’s behavior in litigation to be far from what was promised by spokesman Johnnie Moore in 2016:

Gospel for Asia is 100% focused on continuing its work around the world while working very hard to put an end to the false accusations being continually made against the ministry. Gospel for Asia can document the legal and ethical use of funds donated and clearly answer every question…

As Judge Brooks pointed out in his order, GFA has had many chances to document their use of funds but has stalled all along the way. Now, they face sanctions in federal court and the appointment of a Special Master.

Obviously, Gospel for Asia founder and CEO K.P. Yohannan wants people to believe he doesn’t sit on any boards of Believers’ Eastern Church in India. Even though he is the Metropolitan Bishop of the church, he told his own staff and the Evangelical Council for Financial Accountability that he wasn’t in authority. Now I have found a financial statement filed in the UK where he claims he isn’t on BEC’s board (see note 10). See below:

10 TRANSACTIONS WITH DIRECTORS/TRUSTEES AND RELATED PARTIES

During the period, none of the Trustees of GFA World received emuneration from the Charity (2015 anil).

On 18th October 2016 a donation of F1,660,000 was made to Believers Church India to further the Charity’s objectives. Kadappilaril Yohannan Punnose, is Metropolitan Bishop of Believers Church, which is GFA World’s primary recipient of funds. Whilst he does not sit on the Board of Believers Church and receives no remuneration from Believers Church, he does exercise spiritual oversight through his role as a member of Believers Church’s Council of Bishops. Daniel Punnose is the son of Kadappilaril Yohannan Punnose and is an ordained minister and is a Bishop of Believers Church (among many), but has no formal leadership role in Asia. He is not on the Board of Believers Church and receives no remuneration from Believers Church India.

Gospel for Asia (US) funded a number of radio broadcasts in the UK and provided some administrative support for many of the appeals and communications with supporters in the UK. Kadappilaril Yohannan Punnose and Daniel Punnose are both members of the Board of Gospel for Asia (US) and received remuneration from Gospel for Asia (US) for their services.

On 24th May 2016 a donation was made to Gospel For Asia (US) for 282,000 for two months of “Road to Reality” radio broadcasts in the US. Two of the trustees of GFA World are also trustees of Gospel for Asia (US), and as such were not present in the meeting where the decision was made to make the grant

FOrmer GFA COO Appeared to Admit What Seems Obvious

In a February hearing, an email from former Gospel for Asia COO David Carroll to Yohannan was quoted by attorney Marc Stanley. Atty Stanley represents Garland and Phyllis Murphy who are suing GFA and various officers of the organization alleging fraud and misuse of funds. In this citation, Carroll reminds Yohannan that they have told the public Yohannan has nothing to do with finances and is only the spiritual head but implies such a representation isn’t true.

We can say all we want that we don’t have anything to do with the Believers Church or the field and that you are only the spiritual head of the church and that finances are handled by others but you, but as a practical

matter, that will not hold up.

To the charity commission of the UK, GFA World with K.P. Yohannan sitting on the board, again claimed something that is contradicted by the organization’s founding trust documents, the church’s constitution, and many court documents in India. More recently, we have this statement from a former COO.

Perhaps, there is an explanation. The burden is on GFA and Rev. Yohannan to offer it.

This post is the second in a series covering a February hearing in Murphy v. Gospel for Asia. Former donors, Garland and Phyllis Murphy are suing the leaders of Gospel for Asia in federal court claiming that GFA did not use donor funds as donors intended. Recently, the transcript of the hearing became available. If you are a GFA donor or are thinking about being one, you should read it. It is available via this link with commentary in my first post on the topic. This post discloses the concerns GFA leaders had about being investigated even as they were telling the public they were no problems.

One of the bombshell revelations in the February hearing is the disclosure of an email from David Carroll to K.P. Yohannan which suggests that both men may have misled GFA staff members in May 2015. The Murphys’ attorney Mark Stanley read the email into the record. According to Stanley, in May 2015 then GFA COO David Carroll wrote to GFA founder K.P. Yohannan about his concerns over financial reports and truthfulness. From page 64 to page 68 of the transcript, attorney Stanley cited the email with his comments interspersed throughout. David Carroll’s words are in quotes. I have reproduced Stanley’s testimony below.

MR. STANLEY: What’s really interesting to me also, if I might just take one second and read pretty much one of the key documents in the case. This is an e-mail from Reverend Carroll, David Carroll, to K. P. Yohannan, and I think it’s really important because it really will put it back into perspective what’s going on: “Sir, I need to share with you where I am over this situation.” I’m right here. “I will try to summarize for brevity sake. We have a saying in our country: The numbers don’t lie. The published FC-6 reports” — which they rely on quite a bit in their answers, if you recall — “show westerners that we have either sent money to the field raised for National Ministries and Bridge of Hope to fund the hospital and the corpus fund, or our FC-6 filings are filed wrong. Either way, this is a huge problem. It appears to those reading these that we might have been dishonest to the donors (fraud), or been dishonest to the Indian government, (a PR nightmare at least). Sister Siny’s report below will, in my opinion, do little to satisfy those who are printing out and analyzing our FC-6 reports. I am sorry for not expressing more confidence than this. I think we may have used money raised for National Ministries and Bridge of Hope for the hospital,” [Stanley remarks] which they told us did not happen.

“I think that India feels that we raise money and send it” –[Stanley remarks] by the way, Mr. Mowrey said that in a prior hearing, that none of the money went to the hospital. “I think that India feels that we raised money and sent it to them and they can legally use it any way they deem fit. I hope that I am wrong, but I am doubtful.” [Stanley remarks] This doesn’t sound like someone who has already got accountability, knowing how they spent the money.

“I also don’t think that it is an intentional wrong, but if I am correct, it is a huge wrong. We’ve spoken at hundreds of churches with tears asking for the National Ministries and Bridge of Hope support, and the FC-6 that is public says that we sent much of that money for the hospital and the reserve corpus funds.” Next page.

MR. MOWREY: Could he read the rest of that letter, your Honor?

MR. STANLEY: I am.

MR. MOWREY: Okay. Good.

MR. STANLEY: “It doesn’t matter that we have now moved the money out of the corpus fund” — [Stanley remarks] this is now after the ECFA thing — “because of public FC-6 reports” — I’m sorry. It’s backwards. Sorry. That’s not right, either. That’s right.

“It doesn’t matter that we have now moved the money out of the corpus fund because according to the public FC-6 reports, we have been building them up for years. Moving the money only serves to confirm the feelings of guilt to outsiders.”

Again, they have not been spending the money. They have been building up the corpus funds for years. “I think the only way for us to handle the inquiries raised by Bruce and others is to refer them to our Indian office. Mr. Throckmorton” — that’s the blogger — “(unless a miracle happens) will get this information and may even begin an investigation of us. We can say all we want that we don’t have anything to do with the Believers Church or the field and that you are only the spiritual head of the church and that finances are handled by others but you, but as a practical matter, that will not hold up. Can the field find a way out of this situation? I too am very nervous.”

“I have always believed in total accountability of the field, yet the FC-6 reports provide numbers that, as a former auditor, I cannot just explain away with a simple explanation. I, and the world, will need numerical proof now, and I do not have the ability to get it from the USA end. Only the field can explain it, and I am in the hot seat in this crisis and I feel a lot of pressure.”

[Stanley remarks] I would point out, Judge, this was in 2015, May of 2015, almost three years ago. You pointed out that our discovery was served in August. ECFA asked them for this information in May of 2015. They’ve had three years to compile this information, and they just don’t have it because it doesn’t exist. Nobody ever tracked the designations because they were simply spent out on the — once they were sent to the field, they were done with it. There was no accountability. It goes on to say, “If I say, well, it is not my problem, it’s a field problem, it’s as good as saying we are guilty of misappropriation,” [Stanley remarks] which is true. If I say “The FC-6 reports are filed inaccurately on purpose, due to the hostile environments we work in, it gets the field in trouble and turns the attention to them. I get the feeling that, although we are not financially dishonest, we are financially reckless. The stockpiling of money in the RBC — [Stanley remarks] Royal Bank of India account — “and then the hurried transferring of it to the field, the Hong Kong account, et cetera. Sir, may I please have my name taken off of the RBC account as soon as possible?”

First, let me say that a miracle didn’t happen, if you know what I mean.

David Carroll expressed anxiety about accountability in this email. He acknowledged that either donor funds were diverted from Bridge of Hope and National Ministries to the Believers’ Church Medical Center or the reports were filed incorrectly with the Indian government. There seems to be little doubt that the funds were used for the hospital as I first reported in May 2015. Carroll was fearful that Bruce Morrison and/or I would launch an investigation into the obvious discrepancies. He was right about that. In response to us, he refused to answer any questions and denied any problems.

Furthermore, in a telling admission, Carroll said to Yohannan:

We can say all we want that we don’t have anything to do with the Believers Church or the field and that you are only the spiritual head of the church and that finances are handled by others but you, but as a practical matter, that will not hold up.

GFA leaders told ECFA that they had no control over Believers Church. See yesterday’s post for a run down of what GFA told ECFA about that. In addition, K.P. Yohannan told his Texas staff in May 2015 that he didn’t sit on any boards and had no authority in India. David Carroll was sitting right beside him. This email suggests that he knew it wasn’t accurate when Yohannan said it.

Publicly, GFA said they were operating in accord with the law, ECFA standards, and best practices. However, behind the scenes we now learn that there was worry, pressure, and a more candid assessment of the situation even as the confident and sunny messages were being disseminated to the staff and to the public. I wonder if they knew all along that it was illegal to send cash into India through student backpacks, thus exposing college students to criminal charges.

On February 16, 2018 a hearing was held in Fayetteville AR before federal Judge Timothy Brooks in the case of former GFA donors Garland and

Admirer kissing the hand of K.P. Yohannan. From his 2017 birthday video.

Phylliss Murphy v. Gospel for Asia, K.P. Yohannan, Gisela Punnose, David Carroll, and Pat Emerick. The Murphy’s complaint accuses GFA and named defendants of conspiring to defraud donors and misrepresent the way donated funds have been spent.

This hearing was convened to resolve an ongoing dispute regarding the discovery of evidence in the case. While the transcript is long (over 90 pages), if you donate to Gospel for Asia or are considering it, you should read it.

The context for the hearing is the claim by former GFA donors Garland and Phylliss Murphy that GFA diverted funds away their intended purpose. At this point in the case, the Murphys and their attorneys have requested documents which would demonstrate a link between donations and expenditures. Over several months, GFA attorneys have promised such evidence but have not provided it. The reason Judge Brooks called the hearing was to resolve the situation.

Judge Brooks actually asked the following question in the hearing:

I’ve next got a question for everyone. Will you please raise your hand if you’ve ever seen the movie “Groundhog Day.”

He explained:

I feel like I am Phil Connors who was portrayed by Bill Murray in the movie “Groundhog Day” in dealing with this discovery dispute; and I am of the view, having read the motion and the response, that the defendants, at least in their answers — their answer to these requests for admissions, and in their response to the motion for sanctions, are like all of the people that Phil Connors was dealing with in the movie “Groundhog Day.”

He woke up every day repeating February 2nd, over and over again, but the people that he was interacting with in the plot of this movie didn’t realize that; and I feel like when I read the defendants’ answers and when I read their response that it is as if this Court had not already addressed and ruled on some of these same issues at least twice, if not more and, yet, here we are again.

Judge Brooks had already ruled twice that GFA needed to produced documents in response to questions from the Murphys about where money was spent. They have failed to do so. By this hearing, Judge Brooks summarized the situation:

Plaintiffs now once again seek answers to the same questions that they’ve been asking for months: Was donated money diverted to other causes and do defendants have information or documents that would prove how the money was spent.

This is the crux of the case. If GFA defendants would like to clear their name, they could produce evidence which shows how donations were spent. They haven’t done so. As I pointed out in December of last year, GFA is dragging this out. Anyone who says differently simply isn’t dealing with the case documents.

Donors should ask GFA why a federal judge is exasperated over GFA’s inability to document how donations are spent.

GFA Staff Authorized Transfer of Money from Canada to India to the U.S.

Source TT Architects website

A stunning revelation in this transcript is the disclosure that GFA’s former Chief Operating Officer David Carroll and CEO K.P. Yohannan allegedly had wire authority to move $20 million dollars from India to Texas, presumably for the completion of GFA’s headquarters. Staff were initially told that an anonymous donor gave those funds. Then in May 2015, Carroll told staff that one of GFA’s field partners in India took out a loan for nearly $20 million and sent it to Texas. Carroll and Yohannan told staff that the decision to give the funds was made by the Indian leadership without any influence from Yohannan. According to Yohannan, he had no authority over the decision.

In the February hearing transcript, plaintiffs’ attorney Mark Stanley presented evidence which contradicts this narrative. Here is the relevant portion of Stanley’s testimony.

MR. STANLEY: They [GFA’s attorneys] say that the defendants [GFA] don’t control these third-party entities. I have two documents, if I might — let me find them — showing just the opposite. Here’s one. This document is 2015, April 2015, produced by them from Reverend Dr. K. P. Yohannan, president, asking them to transfer Canadian dollars, or CAD — I don’t know. CAD, those are cash deposits — for Gospel For Asia (India), for further credit to Gospel For Asia (India). These are from — remitting it to the state bank of India in Canada, and I can show you that account number is Gospel For Asia (India). I have the accounts for that. That’s K. P. Yohannan doing that.

David Carroll says he has no control over it. I’ve got David Carroll requesting a document — sorry. There it is. This is David Carroll who says, “I have no control over the field partners,” right? “We have no control; we have nothing to do with them”; yet, David Carroll sends a letter to Sarah Billings from the Royal Bank of Canada asking them to transfer $20 million from Gospel For Asia (India) to GFA’s account in the United States, signed David Carroll, CEO, Gospel For Asia. How could he authorize money coming out of a Gospel For Asia (India) account? We know it’s a Gospel For Asia (India) account because it’s account number — 489 is the last four digits. Here it is. There’s a statement from the Royal Bank of Canada, Gospel For Asia (India), care of Teresa Chupp, in Carrollton — that’s their old address before they moved to Wills Point — for Gospel For Asia (India), and there’s the account number.

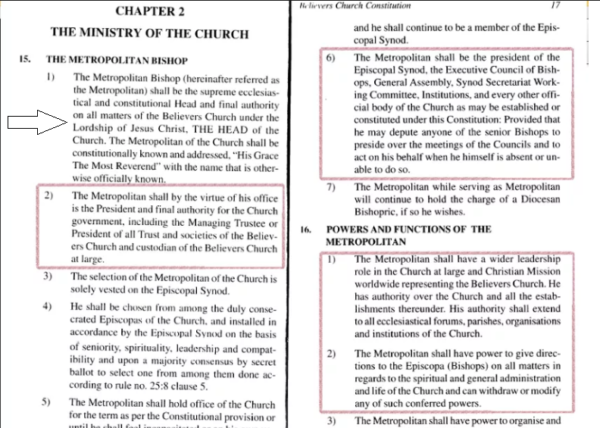

So clearly the spin that they have been told that these folks have no control over the field partners is simply not true. They have control over it. They have wire instructions, wire authority. K. P. Yohannan is the metropolitan of that. You read the constitution from prior hearings. It talks about all of his roles in the constitution.

All of these folks, Mr. Carroll, Reverend Carroll, Mr. Emerick, the Reverend Emerick, all the others have sworn total loyalty to K. P. Yohannan. His niece, Siny Punnose also have sworn loyalty to K. P. Yohannan. They have absolute control of that.

According to Stanley, he has documentation that K.P. Yohannan authorized the movement of funds from the Canadian GFA to GFA-India. He also claims documentation of David Carroll authorizing a transfer of $20 million from the India field partner back to the United States organization. If Stanley’s representations are as they seem, this information contradicts what the Evangelical Council for Financial Accountability said they were told by GFA’s leaders and it contradicts what GFA leaders told staff in 2015.

What Did GFA Tell ECFA?

Beginning in May 2015, the ECFA began talking to GFA leaders, some of whom are now defendants in this fraud case, about alleged violations of financial management policies. In contrast to the evidence presented in the February 16, 2018 hearing, GFA told ECFA representatives that GFA leaders in the U.S. had no control over the field partners in India.

From the ECFA letter to GFA:

During our review on June 3, ECFA staff raised questions regarding GFA’s oversight and control of funds sent to foreign field partners. GFA’s staff indicated that the foreign field partners are completely independent organizations and therefore GFA did not exercise any direct control over field partners. GFA staff also indicated that they did not have a foreign grant process in place to oversee the use of funds.

The ECFA letter specifically refers to the near $20-million transfer of cash. From the letter:

GFA’s financial statements do not appropriately report transactions with foreign partners. During our review on June 3, GFA staff indicated that funds transferred to GFA India were actually transferred to a number of related entities instead of the single entity reflected in the 2013 audited financial statements. Additionally, on August 24 we learned that GFA received a $19,778,613 donation from GFA India, which was classified as a related party elsewhere on the 2013 audited financial statements (also see #8 below). On August 27, GFA staff confirmed that this donation was neither disclosed in the footnotes of the 2013 financial statements as a related-party transaction nor to the GFA board of directors. This inconsistency within the financial statements and lack of disclosure to the GFA board of directors about a significant related-party transaction appears to violate ECFA Standards 2, 3, and 6. On July 20, ECFA was informed that GFA engaged a new audit firm and they are in the process of reviewing related-party transactions.

The ECFA report letter then pointed out the impropriety of moving funds from India which had been given originally as donations exclusively for mission work in Asia.

Use of funds restricted for the field for other purposes. On June 3, ECFA discussed GFA’s claim that 100 percent of field funds are sent and used in the field. GFA staff confirmed that this was accurate. On August 24, ECFA was informed that GFA India made a gift to GFA of $19,778,613 in 2013 to complete GFA’s new office. On August 27, GFA’s staff confirmed that the funds relating to this donation were originally received by GFA as gifts restricted for the field and GFA transferred to field partners to fulfill donor restrictions.

Two important issues are raised:

A. Reallocating gifts donated for field purposes and using them to pay for headquarters construction appears to be a violation of ECFA’s Standards 7.2. GFA staff stated in a recorded GFA staff meeting that you approached the field partner and explained that GFA could borrow the funds in the U.S., at less than desirable terms, for the headquarters construction. However, a gift from the field partner, in lieu of GFA borrowing the funds, would allow GFA to complete the new headquarters and thereby save interest. Therefore, GFA would be able to send more money to the field in future years. ECFA believes that the potential savings resulting from the GFA India gift is an inadequate basis to reallocate gifts donated for field purposes.

B. Reallocating gifts donated for field purposes contradicts GFA’s claim that 100 percent of funds are sent to the field. In fact, a significant amount of donations restricted for the field made a circuitous trip back to GFA and were used for the headquarters construction, as though they had never gone to the field. This appears to be a violation of Standard 7.1.

In a GFA staff meeting, GFA indicated the field partner took out a loan to cover the use of the $19,778,613 gift and GFA staff confirmed on August 27 that India-generated income was used to repay the loan. Our review of the board minutes did not indicate the GFA board had approved, or even been notified, of the $19,778,613 reallocation of donor-restricted gifts.

Now we learn from attorney Stanley that the funds may have simply been transferred by GFA leaders in the U.S. from GFA-India’s Royal Bank of Canada account. Was the office complex finished via a gift from GFA-India? Or did GFA defendants simply transfer $20-million of donor money from one account to another? In either case, plaintiffs attorney presented evidence to allege that GFA leaders had sufficient control to authorize the transfer of funds which were not subsequently spent as intended by donors.

Other Misrepresentations Revealed

There are other revelations in this transcript which I will detail in future posts. For now, I will conclude by repeating my advice to donors to read this document as well as the ECFA report. Some of the same issues which led to the removal of GFA from the ECFA membership are still current today and have come to the attention of the presiding federal judge in this case. Although the trial isn’t slated until next year, consumers and donors can use the evidence available to make their own judgments now.

In a May 14 2015 staff meeting, a Gospel for Asia staffer asked why GFA regularly asked for funds since so much money was just sitting in banks in India. I understand the point of the question. If GFA has millions sitting in banks unspent, then why bother donors for more money? To answer, GFA officials complained that all funds have to be spent on donor designations which can be tracked here and in India. This question and the answer are relevant because in the current RICO lawsuit, GFA defendants are now saying they are having great difficulty tracking down where the U.S. donations are spent. Questions about how funds have been spent are at the center of the federal fraud case brought by Garland and Phyllis Murphy against GFA.

GFA Told to Produce Documents

In a February court order, federal judge Timothy Brooks scolded GFA for insufficient answers to requests from plaintiffs for answers to questions about where funds have been spent. Specifically, Brooks wrote:

Furthermore, despite consistently telling donors for years that 100 percent of donations went for the purposes designated, now attorneys for GFA want to revise history. In the February 28 order, Judge Brooks summarized the discovery process and pointed out that GFA had originally promised to account for specific donations, but then noted that GFA had backed away from that stance (see footnote below). If GFA now claims they never promised to use donations for designated purposes, they will need to explain this very clear message to staff on May 14, 2015. In that meeting (a link to the audio is below), K.P. Yohannan and David Carroll said donations made for specific items were held until those items could be purchased. Carroll also added that GFA in Asia had reports to verify these expenditures.

GFA Staff Q&A Meeting

In this meeting, GFA founder, CEO, and Metropolitan Bishop of the Believers’ Church K.P. Yohannan, then COO David Carroll, and other leaders K.P. Yohannan, source: Youtube

addressed staff questions about controversies just beginning to swirl around GFA. To listen to the entire exchange, click through to the audio. Because GFA has threatened Patheos with legal action on previous occasions, I am hosting the audio elsewhere and will describe it below.

Initially, David Carroll read this question: “We always pray for more funds because we say the ministry could do so much more if we had it. Why is the ministry sitting on so much in India ($94 million per FC-6 reports)?” Carroll explained that the FC-6 reports are not audited financial statements and are required to show what money comes into India. He said GFA-USA has nothing to do with the preparation of the report.

He then said the funds going into India are restricted and have to sit in an account until the use can be fulfilled. He used the example of donations for bicycles. Funds given for bicycles have to sit in an account until they can spend the money on bicycles according to Indian law. Even if an earthquake happens in Nepal and funds are needed, those bicycle funds can’t be used for earthquake relief.

He said the balance in India was about $7 million, not the $94 million claimed by the questioner.

He said, “We cannot spend the money until we can spend it on the project for which it was designated and that’s important.”

Yohannan declared, “Absolutely every designation is fulfilled. If not, the guys who are responsible for it, the guys in India, they go to jail.”

Carroll finished the question by saying:

As a former auditor, I’m always wondering, so did the money that someone gave for a blanket for a cold person in North India, is that sitting somewhere, does somebody know about that blanket that’s given like that amount? And we’ve asked that question of our Asian office and they’ve said, ‘yes, we actually have a report that mirrors your report here.’ So yes, if a blanket was given here but it hasn’t yet been given because it’s warmer there or whatever the reason, then the money is sitting there and able to be accounted for when it goes out.

Why Is It So Hard Now?

When reassuring staff in 2015 that donations were being used as promised, GFA leaders were quite convincing. When addressing discovery in a 2018 RICO case, a federal judge appears to be frustrated with GFA’s inability to do what they promised. These inconsistencies were exposed months after the May 2015 staff meeting.

Later in 2015, the Evangelical Council for Financial Accountability did an investigation which ended with the expulsion of GFA from membership. In their September 2015 report*, the ECFA found that the GFA’s field partners banked foreign contributions for years while local funds went to meet designation from donors. Because of this procedure it was “extremely difficult for GFA to demonstrate that it has exercised appropriate control of the funds” donated by U.S. donors.

David Carroll told staff that GFA’s field partners had $7 million on account. ECFA’s report found the amount to be $186 million at about the time of the staff meeting. From the ECFA report:

Allegations were made that GFA had upwards of $150 million in partner field accounts, far more than necessary to provide appropriate operating reserves. During our visit on June 3, ECFA was informed that GFA field partner cash reserves were approximately $7 million. After ECFA requested detailed documentation of cash balances held by foreign field offices, on June 29, we discovered that GFA’s field partners had $259,437,098 on hand at March 31, 2014 and approximately $186 million in June 2015.

In the ECFA report, GFA acknowledged that solicitations are more specific than expenditures. I wonder if GFA’s attorneys have read this report.

GFA solicits funds for narrower purposes than the eventual expenditure of the funds. During ECFA’s review on August 12, GFA staff provided a document to demonstrate the flow of funds from GFA to field partners. ECFA learned that donor-restricted donations are appropriately tracked by particular revenue classifications. However, we also discovered, and it was confirmed by GFA staff, that the disbursement of the gifts are tracked in much broader categories. For example, donations were received and tracked for 38 different specific items including kerosene lanterns, bio sand filters, chickens, manual sewing machines, blankets, bicycle rickshaws, and others, but related expenses were only tracked as “community development.” In other words, donations were raised for 38 specific items, with the donations pooled for expenditure purposes instead of expending them specifically for the purposes raised.

ECFA did not find any evidence that donors to the 38 different giving categories had awareness that their gifts were grouped and used in a broader category than the specific categories in which the gifts were raised. ECFA’s staff raised concerns regarding GFA’s compliance with ECFA Standard 4, 7.1, and 7.2 in raising funds for a particular purpose but then failing to document the actual use of those funds by the particular donor-restricted purpose.

Subsequent to this conversation, on August 16, GFA staff indicated that GFA field partners will begin tracking expenditures by specific item accounts to provide adequate transparency as to the use of designated funds.

*This report was not made public by the ECFA or GFA, but was released to me by Gayle Erwin, former GFA board member who resigned from the GFA board over GFA’s misconduct.

{kind=link}