Bruce Morrison is a pastor in New Glasgow, Nova Scotia, Canada. For 20 years, Morrison’s church supported Gospel for Asia but stopped doing so in April of this year. Now, in a 13 page letter, Morrison details the reasons for ending support and provides insight into his efforts to get answers from GFA.

Morrison’s findings are very similar to my own. While we have spoken some over the past several weeks, Morrison began looking into GFA’s finances about a month before I did. His church dropped support about the time I began writing about GFA and came as the result of his research and efforts to get answers from GFA.

Read Morrison’s letter with the knowledge in mind that his church supported GFA for 20 years. It is hard to believe that a church with that track record would be unable to get basic answers from a mission organization. However, given my experience with GFA, I certainly believe it. The lack of information and answers should be a red flag to current and prospective donors.

Silence is complicity

Morrison writes with concern for other churches. After asserting that “stories of abuse at the hands of spiritual leaders are far more common than they should be,” Morrison writes:

It is with both a sense of reluctance, but also of moral responsibility, that I write this letter to the larger body of Christ. Reluctance – from the unpleasantness of speaking about the need for correction in a Christian ministry, and responsibility – since silence in instances such as I will describe herein is complicity.

If GFA has answers to the issues which Morrison raises, it it beyond my understanding why they have not offered them. Specifically, Morrison wants an explanation of why foreign contributions to India for 2013 in the amount of $43.48 million do not show up in Indian records. He wants to know why over $150 million was sitting in Indian banks at the end of FY 2013. He wants to know if GFA got written permission from donors to bank around $50 million in a corpus fund. There are many other questions as well. I have been raising these same questions independently since April.

This is getting interesting.

On Tuesday afternoon, I contacted Bland Garvey, the accounting firm which did Gospel for Asia’s 2013 audit. I wanted to know if BG had been retained to do GFA’s 2014 audit and perhaps learn why the audit is not out yet. As I understand it, GFA has to turn in an audited financial statement by July 31 to the Evangelical Council for Financial Accountability as a part of the requirements for membership. GFA is a charter member of ECFA. GFA has been referring to the organization’s membership in ECFA as a means of deflecting questions unaccounted for funds and so it is probably important to protect that membership.

When I called BG, I was referred to attorney Gary Kessler. I called and wrote Attorney Kessler with the following questions:

Is Bland Garvey doing the 2014 audit for Gospel for Asia? If not, why not?

If so, will BG correct the misstatements from the 2013 audit that GFA-US only gave money to GFA India and several other GFAs in Asia when in fact GFA-US also gave money to three other NGOs?

The amount of money GFA said they donated to GFA-India is millions more than what GFA-India reported to the Indian govt. Will BG mention this discrepancy?

Last years audit was complete by June 13; this years is much later. If BG is doing the audit then why has this audit been delayed.

He wrote back with the following:

Mr. Throckmorton,

Applicable law prevents a CPA from communicating the information you requested. I advise you to contact Gospel For Asia and obtain the information you seek.

Thank you.

Gary

I wrote back asking for citation of TX law that forbids BG from acknowledging their auditing relationship with GFA and asked if he was representing BG in any litigation. He wrote back to say:

Please contact Gospel for Asia for any information you desire regarding the organization. I will not be responding to any more of your requests.

Thank you.

Gary

And so Mr. Kessler joined a growing list of people from Texas who don’t want to talk to me.

Having looked at the CPA law, I can understand why BG cannot address all of my questions. However, just telling me that they are doing GFA’s audit isn’t as clear cut to me. According to TX law, if BG has told the anyone in the public that GFA is an audit client, then they are not required to withhold information. See this clause:

The provisions contained in subsection (a) of this section do not prohibit the disclosure of information already made public, including information disclosed to others not having a confidential communications relationship with the client or authorized representative of the client.

I already know BG did the 2013 audit so I know there was a relationship. And it is possible that others not now affiliated with GFA know if BG is auditing the books. This should be known soon enough because that audit should be available to the public if GFA wants to remain a member of ECFA. That is, of course, unless ECFA gives GFA a pass. Hopefully, then we will know if GFA corrects the misstatements in the 2013 audit.

What puzzles me is why BG didn’t just tell me that but instead referred me to an attorney who in turn referred me to GFA.

On May 7, 2015 Gospel for Asia’s Chief Operating Officer David Carroll told me he would no longer answer any more of my questions. Leading up to that email was my question about why funds given and reported outside of India didn’t show up in Indian records. Specifically at that time, I asked about the funds (15 million Canadian dollars) declared in Canada as being sent to India in 2013 but never reported as being contributed from a foreign source as required by Indian law (I later wrote about that discrepancy). My email from May 5 was as follows:

David – I have reviewed some information available to Canadians regarding charities. In the year most recently available, filings with the Canadian govt. show 15million to India.

In the same year in India, govt forms show nothing came in from Canada.

Can you account for this discrepancy? I intend to write about this tomorrow afternoon.

Thank you, Warren

On May 6, Carroll wrote back:

Good morning, Mr. Throckmorton,

The Canadian funds were combined with U.S. funds by our auditor in India for various accounting reasons. There is no requirement that they be reported separately.

Thank you.

David

That same day, I wrote back with follow up questions and a request for information.

David – Can you provide contact information for your auditor in India? This combination of funds appears to be in violation of Canadian law, and possibly Indian law, according to my sources. I would like to understand the auditor’s rationale for believing there is no rationale for these sources to be reported separately.

Thanks, Warren

On May 7, Carroll cut off contact.

Warren,

No, Gospel for Asia has not violated the law.

When you first contacted us, I mentioned that we would not be able to respond to every question you put before us. Now, with the increased volume and frequency of your questions, it has become clear that this back and forth has become a distraction from our mission work. For this reason, this will be my final response. We understand that you will continue to explore issues around Gospel for Asia and continue to be fed accusations from former employees, and we accept that.

We continue to remain accountable to all applicable laws and regulations, to the Evangelical Council for Financial Accountability and to independent auditors.

Sincerely,

David

In my post on the Canadian funds, I made sure GFA’s position was included. I would have included more if GFA had provided it. Instead I got my hand smacked and was sent to time out.

I have written GFA several times since then. I have addressed correspondence to Carroll, John Beers, and K.P. Yohannan. I have sent some of the emails to the Evangelical Council for Financial Accountability. No answers.

In light of my efforts to get answers from GFA, imagine my surprise when I heard from former donors that GFA is saying they tried to work with me but have been advised by their financial consultants (?) not to talk to me. I wrote David Carroll yesterday to ask him if GFA reps are telling donors that GFA tried to work with me. Apparently still taking his financial consultants’ advise, there has been no reply.

GFA, according to several former donors, you are telling them that the reason you can’t disclose answers to the question posed here is because I am asking about funds going to high risk areas for persecution. We both know that isn’t a plausible answer since no identities or activities would be disclosed by answers to the questions I have asked.

GFA, if you are telling donors that you have tried to work with me, please stop. We both know better. I am willing to look at any new information you provide. You know it isn’t just me asking these questions. Pastors are asking, donors are asking, staff are asking, former staff are asking. If you really want to work with me, you have my contact information.

The following issues would be a good start:

GFA’s audit (conducted by Bland Garvey) failed to disclose three related NGOs which received funds from GFA’s American donors. Furthermore, between $30-50 million of money GFA said went to India in 2013 does not show up in reports submitted to the Indian government. Similar gaps show up in 2012 and other years.

Why does GFA maintain a massive surplus of funds (around $150 million) being held in Indian banks, subject to major devaluation of the rupee?

An ongoing concern has been the stories of around 100 former staff members who have unresolved problems with GFA. Current turnover in U.S. staff should be a red flag to any supporter. Reports are now that few students are returning to the School of Discipleship for a second year. Is that true and what will that do to your tax exempt status if there are no students?

GFA reps and the ECFA have never explained why GFA–India did not disclose to the Indian government the $15 million given to GFA–India by Canadian donors in 2013.

Why did K.P. Yohannan claim he didn’t allow men being ordained in Believers’ Church to kiss his ring but a video shows the men kissing his ring during a ceremony.

In 2014, an Indian tax court considered a claim against Gospel for Asia and Believers’ Church. According to a court filing dated December 12, 2014, Gospel for Asia and Believers Church spent more of their income than allowed on purposes not related to the reason they were formed. Doing so made that income taxable. Gospel for Asia and Believers’ Church together appealed the assessment of tax, saying that the use of the funds were given to related organizations which had charitable purposes. The court found that funds were still being used for unintended purposes and remanded the matter back to the tax assessor. I have been unable to find any documentation of how much GFA and BC had to pay or if the matter has been resolved.

You can read the whole thing at this Indian site where public records are archived. I have pulled out the relevant portions below:

Shri M Anil Kumar, the ld.DR submitted that both the assessees are registered as charitable trust u/s 12AA of the Act. During the year under consideration, the assessing officer found that both the assessees have given loan to other trusts from the unutilised portion of the income which exceeded more than 15%. Referring to section 13(1)(d)(i) of the Act, the ld.DR submitted that the assessee trust invested its funds in the form/mode otherwise than prescribed in section 11(5) of the Act. Therefore, according to the ld.DR, there was violation of section 11(2) r.w.s. 13(2)(d) of the Act. According to the ld.DR, the assessee is not entitled for any exemption.

Assessees refer to Believers’ Church and Gospel for Asia. Both are registered as charitable trusts. Both groups had income during the 2010-2011 tax year and loaned more than the allowed 15% to other charitable trusts related to GFA and BC. Originally, the tax assessor considered those loans improper investments which meant that the income invested was not exempted from tax. The original complaint of the tax assessor was eventually set aside in favor of another interpretation by the tax court and remanded back to the tax assessor for reassessment of tax.

GFA and BC had the following interpretation of tax law. The “ld.representative for the assessee” refers to GFA’s and BC’s representative.

On the contrary, Shri Venkitachalam, the ld.representative for the assessee submitted that both the assessees advanced funds to other registered trusts which have similar objects. According to the ld.representative, the assessee advanced funds to BCMET for construction of hospital building. BCMET is also a registered trust u/s 12AA of the Act. The ld.representative further submitted that Carmel Education Trust also a registered charitable trust u/s 12A of the Act was given funds by the assessee to carry out their charitable activities. According to the ld.representative, when the funds were advanced to other similarly placed charitable trusts, amounts to application of income; therefore, the provisions of section 11(2) are not applicable. The ld.representative further submitted that advancing money to similarly placed charitable trusts does not amount to investment or deposit. Therefore, there is no violation of section 11(5) of the Act also.

GFA and BC “advanced funds” to related trusts, one involved in building Believers Church Medical College Hospital and the other an educational trust which operates various schools. I don’t know for certain, but it sounds like the educational trust was given funds to help fund operating expenses. The BC’s hospital was given money for construction of the state of the art facility. Thus, BC and GFA took income on donor money and used it to fund the hospital and engineering school.

The court considered both sides and concluded that “substantial income” of GFA and BC was not used for “the purposes for which they were formed.”

We have considered the rival submissions on either side and also perused the material available on record. It is not in dispute that substantial income of the assessee trust was not used by both the assessees for the purposes for which they were formed. (emphasis added)

The court said there is no question that GFA and BC misused the funds. The main question was about how to treat those funds for tax purposes. After going through an evaluation of Indian law relating to the facts of the case, the court ruled as follows:

Therefore, in view of the latest development of law with effect from 01-04-2003 if the income is paid or credited to another trust or institution even though they are registered u/s 12AA or approved u/s 10(23C) of the Act, the same has to be treated as income of the assessee.

Believers’ Church Hospital and Medical College

Since GFA and BC loaned/advanced more than allowed by law, that income has to be treated as income of the two organizations. The court then sent the matter back to the tax assessor to figure out what GFA and BC owed.

I can’t find any additional cases or appeals so the matter might still be active. I asked GFA what happened in the case but, as usual, received no answers.

Donors have questions but all they are getting are assurances that their donations are going for the purposes intended. This case provides one more basis to question that claim.

This case adds one more item to the growing list of concerns about GFA’s financial affairs.

This seems like an odd way to evangelize.

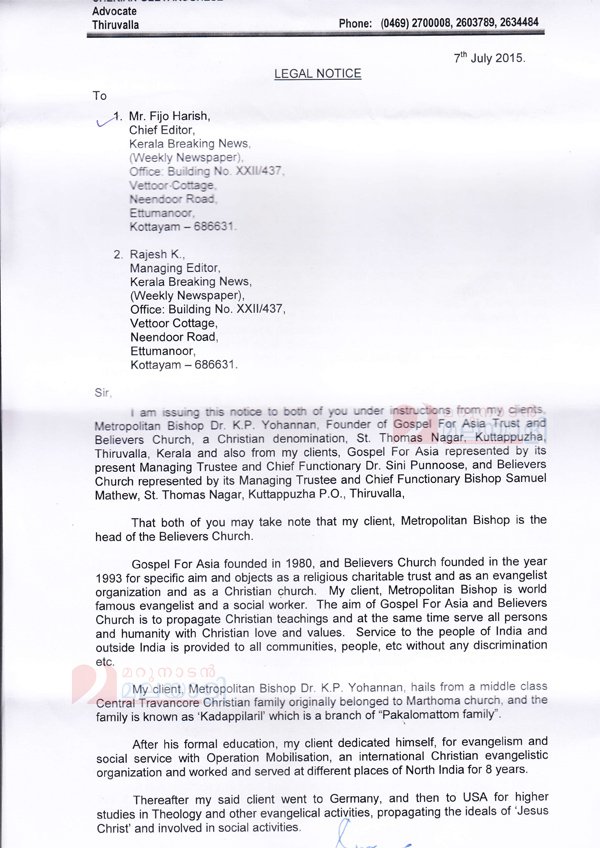

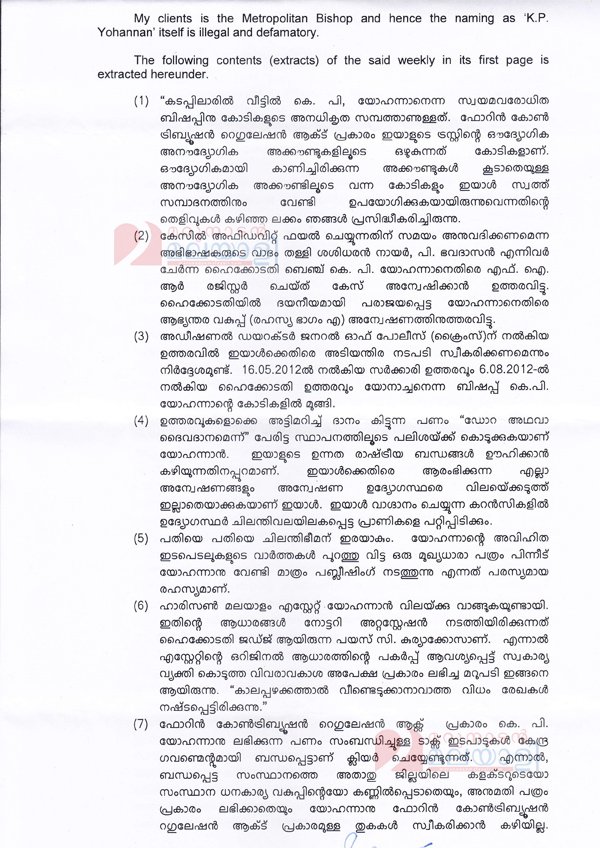

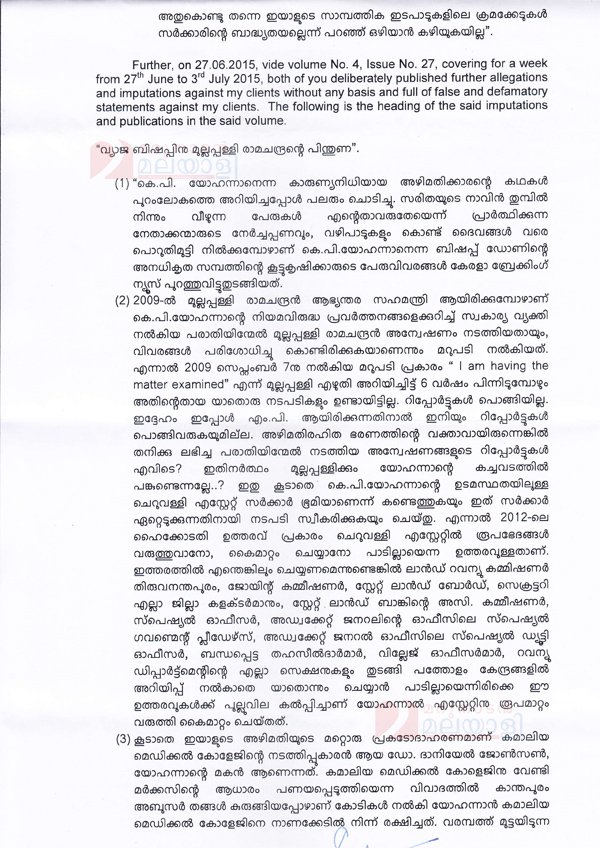

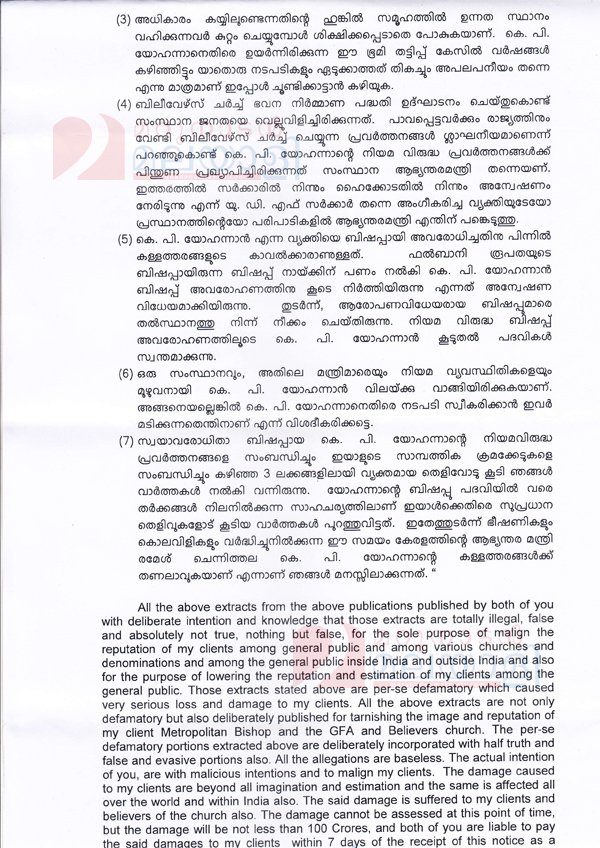

I can’t read the Malayalam but the English indicates that GFA-India and Believers’ Church are threatening (or have filed, I can’t tell for sure) a defamation suit against a paper in Kerala India (“Breaking News Weekly”). If this is accurate, GFA-India and Believers’ Church are demanding $15.7 million for defamation which includes calling K.P. Yohannan by his name instead of referring to him as Metropolitan Bishop.

I am seeking a translation but for now here is the “legal notice” according to the paper.

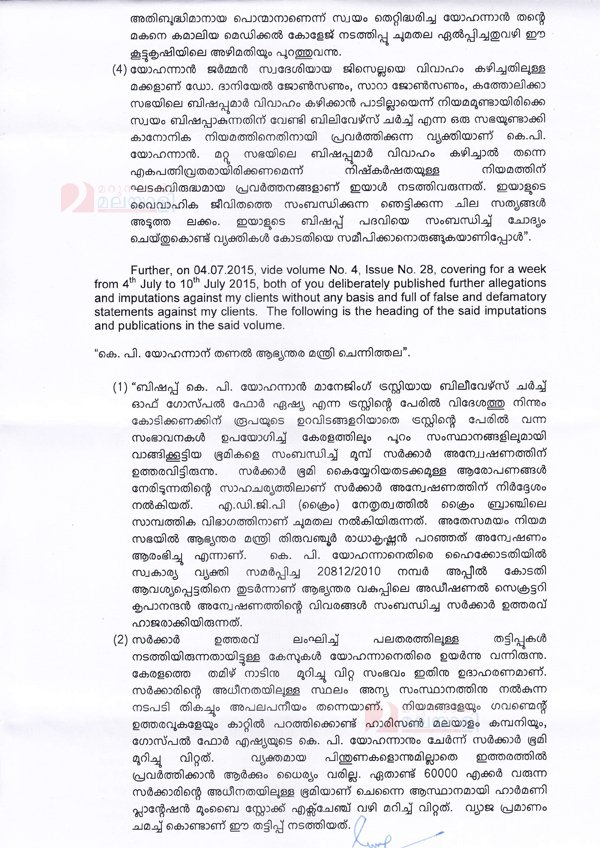

Note that the letter says calling K.P. Yohannan by his name is defamation. He apparently is to be addressed as Metropolitan Bishop. The next two pages pull out Malayalam passages from the paper which GFA/Believers’ Church believe to be defamation. Here is page three and four. Page five is below.

This is all that was provided by the Indian newspaper. The amount demanded in U.S. dollars is $15.7 million (100 Crores). The lawyer wants that sum in 7 days.

If this is true, it won’t be the first time GFA/Believers Church have sued in India. You can use this website to read cases where GFA has been sued and has sued various parties in India.