In this months survey, the gap between evangelical insiders in World’s poll and GOP survey respondents remains wide on Donald Trump. No participant in World’s survey chose Trump as first choice for president.

Ted Cruz gained ground and Marco Rubio remained first in the results.

As I noted yesterday, it worries me that support for Cruz is rising. His views lean toward the Christian dominionist wing of religion and that is just one reason I believe he cannot appeal to independents and moderates.

His governmental experience is very limited. He was elected to the Senate in 2013 and if elected will have been a Senator about as long as Barack Obama was before his first term. Republicans were rightly worried about Obama’s lack of experience in 2008. Cruz will face the same attacks from the left. In a time when fear seems to be prevailing emotion, Cruz’s thin resume’ does not inspire confidence.

Rubio has a bit more experience in the Senate but much more previous experience in state politics. Of the two, Rubio seems more electable. While he may hold similar positions as Cruz, he articulates them more frequently in general political terms rather than apocalyptic religious ones.

While I have not and probably won’t endorse a candidate until much later in the process, I know what concerns me and I know what I can’t endorse. Right now, Cruz falls into that category.

Month: December 2015

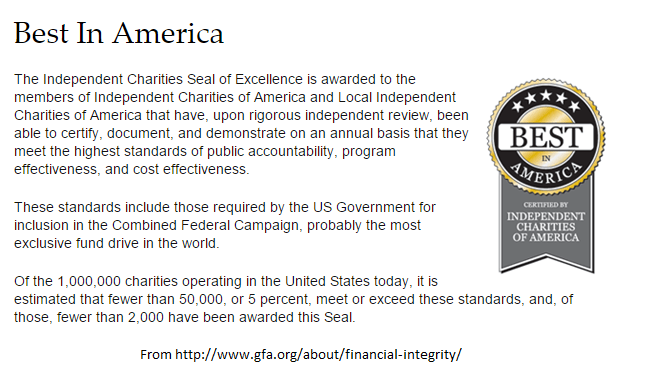

Gospel for Asia Is No Longer a Member of Independent Charities of America

The Seal is gone.

I have confirmed that Gospel for Asia is no longer a member of Independent Charities of America. A representative of the company which manages memberships has indicated that GFA was denied membership last week. As of now, the Best in America Seal of Excellence touted by GFA has been removed from most locations on the GFA website (for some reason, it remains here at the time I wrote this).

I have not been able to learn what triggered ICA’s action. I do know that ICA was aware that the Evangelical Council for Financial Accountability terminated GFA’s membership.

In October, I reviewed the ICA criteria for membership. It seemed to me at the time that GFA did not comply with several ICA standards.

One of the major standards used by ICA is approval by the Office of Personnel Management for participation in the Combined Federal Campaign. I have contacted OPM to inquire if GFA is still an approved charity.

UPDATE: Today a Maguire & Maguire representative alerted me that the reason GFA was denied membership was because they failed to turn in their 2014 audit and their modified 990 form as required by their membership standards. Maguire & Maguire provide management services for the Independent Charities of America.

Remembering the Prophecy About Mark Driscoll’s New Church and Daddy Issues

In late October 2014, just after Mark Driscoll resigned at Mars Hill Church, he showed up at Robert Morris’ Gateway Church pastors conference. He was originally scheduled to speak at the conference but stepped away from the program as the troubles at Mars Hill became more difficult.

In one of the sessions, conference speaker (and apparent co-director of the new The Trinity Church in Phoenix) Jimmy Evans gave a prophecy about Driscoll. According a witness who wrote down the prophecy on an Instagram account, Evans told Driscoll:

You led a great movement as a brother, you will lead a greater one as a father, your later years will surpass your younger.

In a September 3 Q & A session at the Living Springs Grace Association conference in Phoenix, Driscoll provided more detail about the “word from the Lord.” Listen to Driscoll’s description in the first two minutes of this segment of the Q&A (Listen to the entire sermon by going to this amazing website).

Transcript of the first 1:35:

I was trying to make sense of everything that was going on and what I was to learn from it and I was sitting in a pastors conference with a bunch of charismatics and pentecostals because they tend to be the most encouraging and loving I’ve found. And so they invited me just to come and observe and learn and not teach but just to learn and so I was there at this large pastors conference and I’m sitting, you know, near the front row, and I’m just kinda on the verge of losing it all the time, emotional still, and this pastor gets up and says, well before I speak, I have a word for Mark Driscoll, and I was like, aw man, I do not want a word. I just want to sit here and be anonymous and not get the prophetic word. And so, he got up and gave a word that was a word from the Lord and it just cut me to the heart. And what he, the basic gist of what he said was, you left ministry as an angry older brother and you’ll return as a loving father.

And then he pulled me aside afterword in his Ford truck cause that’s where the Shekinah Glory dwells and the good stuff goes down. So we sat in his truck and he said, you started off as a guy who was angry with some bitterness and you attracted a lot of angry bitter young men with father wounds and they picked up on your tone of anger and bitterness.

The prophecy is different in this telling, no doubt influenced by the conversation with Evans in the Ford truck. If this is indeed the Gateway conference word from God, then Evans is helping to bring about his prophecy by partnering with Driscoll with this new venture in Phoenix.

The word of prophecy last October is important now that Driscoll has incorporated a new church apparently with the author of the prophecy. The tone and character of this church will probably be more charismatic and apostolic than Mars Hill. The fulfilling of this “prophetic word” appears to be on the horizon with Driscoll set to return as a spiritual father figure.

In fact, the narrative Driscoll has cultivated is that God has spoken specially to him to get him to this place. Just over a year ago, he was prepared to enter into his elders’ plan for restoration but left that behind because he said God spoke to him and released him from Mars Hill. Now, he returns to ministry as the fulfillment of additional revelation given to Jimmy Evans.

The rest of this audio provides some eyebrow raising commentary by Driscoll on what he perceives to be a massive father wound among young men in America. Driscoll refers to himself as a spiritual father and his wife Grace as a spiritual mother. At 45, he seems to view himself as old.

At 6:21, Driscoll said that he believes

…part of the gifting of apostolic ministry is spiritual parenting. It’s younger leaders looking up and saying that’s like a mom and a dad that I look to and learn from, and I find health and comfort and love under their leadership and in this family of people and churches we look to them in a parental way.

He added that such language can sound cultic if imposed on people. However, because of what he believes is a “massive father wound” in the culture, people learn to look to the pastor and his wife and as parental figures. The rest of his speech dwells on why young men follow “dead guys” like Wesley and Spurgeon. They want distant father figures who do not hold them accountable.

I think some Mars Hill elders might wonder if Driscoll is preaching to himself in the remaining minutes of that speech.

My reaction is that reparenting one’s congregation seems like a prescription for disaster. We have just about put behind us the notion that counselors should reparent clients, I don’t think such a stance should be encouraged among ministers.

In any case, this appeal in September to how he sees his return to ministry might give some clues about the tone and ministry of The Trinity Church. Perhaps, it should have been called My Father’s House or something like that.

News from the Alternative Universe: David Barton Builds Support for Ted Cruz in the Midwest

I confess I didn’t see this coming.

In August 2012, when Thomas Nelson pulled David Barton’s flawed book on Thomas Jefferson, I hoped that the event would cause some reflection among culture warriors about the Christian nation narrative that threatens our First Amendment freedoms. I thought debunking the extreme claims would cause reflection about the real heritage of our nation’s founders and the actual role of religion in that time period.

I now realize I was wrong.

If anything Barton now has more power to spread his alternative view of reality. An article in CNN yesterday drove that awareness home. In it, CNN cites a statement from Barton, who now manages Ted Cruz’s Super PAC.

“As Sen. Ted Cruz is rising in polls nationwide, we are excited to establish and build support for him,” said David Barton, the head of the super PACs, in a statement. “Americans know one of the strengths of our great nation is in the ideals held by Midwesterners.”

It is surreal that Barton is in the position to spend great sums of money to promote a presidential candidate who shares his alternative view of America. Let that sink in. As strange as it seems for me to write this, Cruz could win the nomination. If so, we could have a Christian reconstruction/seven mountains theological hybrid in the White House.

Christian historian friends, are you paying attention?

Update of Charity Review of Gospel for Asia Australia; Are GFAA and GFA Related?

Earlier this year, Ted Sherwood did a charity review of Gospel for Asia Australia. Recently, he updated it. As a part of the update, Sherwood evaluates a rather amazing claim made by an Australian association of Christian ministries called Mission Interlink. In essence, Mission Interlink claims that GFA Australia is independent of GFA in the U.S.

While technically accurate, it is clear from the evidence Sherwood supplies that GFA Australia wouldn’t exist if there was no GFA in the states or in India.

About Mission Interlink’s position, Sherwood wrote:

GFAA is a member of Missions Interlink, the closest we have in Australia to the ECFA:

Member use of the Missions Interlink logo implies high standards of governance and financial accountability, giving the Christian public assurance of their integrity[iii].

On 27 August 2015 I sent a link to my review to the National Director, Pam Thyer, suggesting that GFAA was in breach of one or more of their standards. On 3 December 2015, in response to my suggestion that donors should be alerted to GFAA’s misrepresentation when soliciting donations, Pam said that she had discussed the matters I raised in the review with GFAA and had concluded that ‘they do not contravene the MI Standards’.

Sherwood disagrees and provides evidence that GFA Australia is indeed in violation of some MI standards.

Furthermore, it is incredible that MI sees GFAA as separate from GFA. The only real reason GFAA exists is as a conduit to GFA in India. GFAA is sending money to GFA in India in ways that may or may not align with donor intent. Donors in Australia should be aware that their donations may be used to purchase or develop for profit businesses under the control of Believers’ Church.