Listening to the May 14, 2015 Gospel for Asia staff meeting, I heard K.P. Yohannan say he doesn’t have control or sit on any boards of GFA organizations in other countries. Listen:

Click this link: K.P. Yohannan tells staff he is not on any boards in India

Transcript:

And by the way, just so you know, I am not legally on any boards, any trusts, anything in any of these countries. I have no powers to make decisions or sign money, or release money, or make decisions, I am completely legally…why? Because anybody who work in the United States or overseas countries have a board membership or have legal membership should not be part of their legal entities in India. It’s a conflict of interest and therefore we send the funds and it is immediately under the government watch care and the government of India is responsible and investigative agencies and tax divisions to make sure that is carried out within the time frame or whatever they do, that is a public thing.

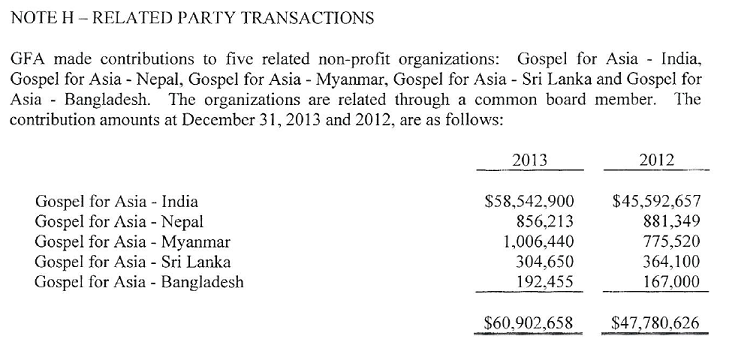

I found this to be an odd declaration since the 2013 financial audit seems to point to a common board member of GFA in the United States and GFA affiliates in India, Nepal, Myanmar, Sri Lanka, and Bangladesh. From the 2013 audit:

If this board member isn’t K.P. Yohannan, then who is it? No matter who it is, by Yohannan’s reasoning, being on both boards would be unethical since Yohannan says having an American board member on the board of an Indian charity which allocates American funds is a conflict of interest.

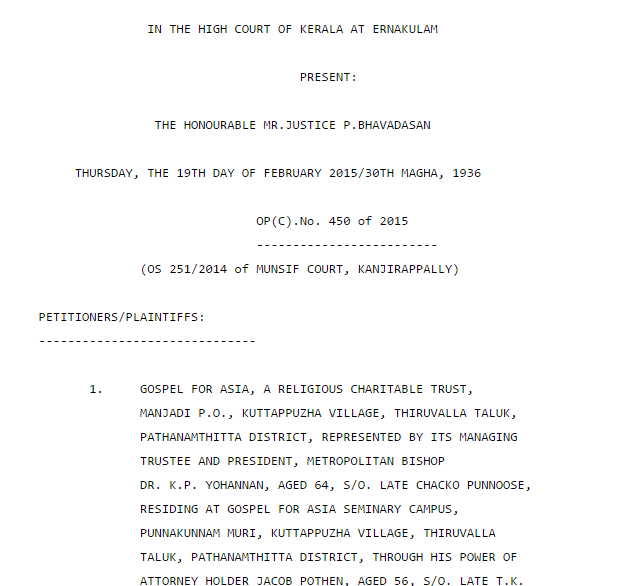

However, it certainly seems as though it is Yohannan. For instance, Yohannan is referred to as a plaintiff in a court case brought by Gospel for Asia in India (click the link to read the case notes). He is also described as the “managing trustee and president” of Gospel for Asia based in Kerala. From the Indian website:

This document is dated February of 2015, just three months before Yohannan told his staff he wasn’t on any boards. There are many other court cases which list him as “mananging trustee and president” of Gospel of Asia (link, link, link, link).

In another lawsuit, Yohannan is listed as the managing trustee of the Carmel Education Trust of the Believers’ Church.

3. Caarmel Education Trust, (Believer’s Church Trust) Represented by its Managing Trustee, Dr.K.P.Yohannan, Caarmel Engineering College, Perunadu,Pin – 689711 (R1 by Adv.K.Venugopalan Nair) (R2 & R3 by Adv.Anilkumar.A.S) APPEAL No.897/2012

In this publication by the state of Kerala in India, Yohannan is referred to as the “Managing Trustee” of the Believers’ Church.

G . O. (Rt.) No. 448/2011/LBR. Thiruvananthapuram, 17th March 2011. Whereas, the Government are of opinion that an industrial dispute exists between Dr. K. P. Yohannan, Managing Trustee, Believers Church India (B. C. I.), Thottabhagam P. O., Thiruvalla and the workman of the above referred establishment Shri Joseph Kizhakkedathu, Manipara P. O., via Uliyikkal, Kannur District-670 705 in respect of matters mentioned in the annexure to this order ; And whereas, in the opinion of Government it is necessary to refer the said industrial dispute for adjudication…(emphasis added)

Yohannan is listed as the patron of the Believers’ Church Medical Cente, the Residential School and the Mahatma School. Why would he be listed as patron if he has nothing to do with determining their funding?

It seems clear that the legal system in India believes that K.P. Yohannan is on the boards and has responsibility for these entities.

Additional Information:

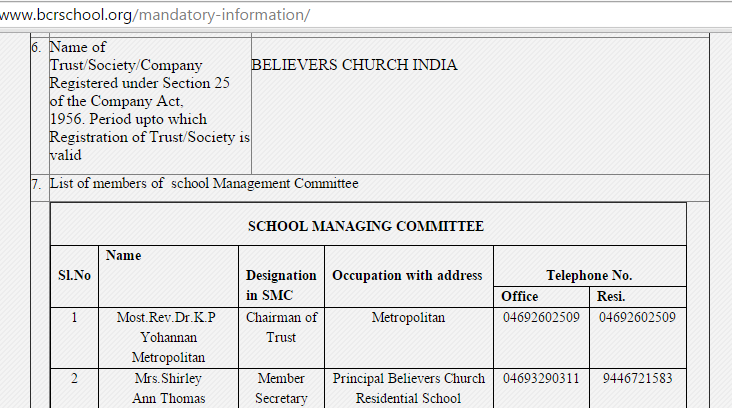

An alert reader posted a link in the comments that K.P. Yohannan is listed as the chairman of the Believers’ Church trust on a page of one of BC’s schools; and of course he is the Metropolitan Bishop of the church. He is president of GFA-US, a group which sent nearly $20 million to Believers’ Church in the FY ending in March 2014. In addition to K.P. Yohannan, Yohannan’s son Daniel sits on both boards (GFA-U.S. and Believers’ Church).

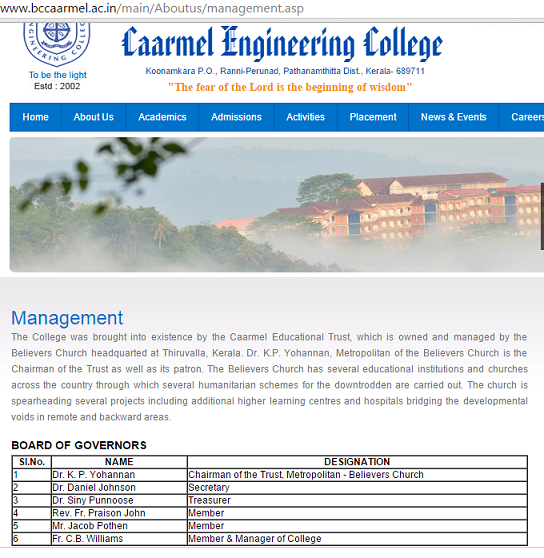

Thanks to another alert reader, we can see that Yohannan and his son are listed as board members of the Believers’ Church Seminary, with K.P. Yohannan being listed as president of the Governing Board. Yohannan is also listed on the Caarmel Engineering School as the chairman of the Believers’ Church trust.

All of these listings are current.