During the late 1990s, I served on the board of the American Mental Health Counselors Association. One of the first things we learned as new board members was the concept of fiduciary responsibility. I learned that our organization was formed to serve the interests of our constituents and more broadly the public interest. I also learned that I was responsible to ensure that the organization functioned within the law and in accord with rules we set for ourselves (e.g., by-laws). Furthermore, I had a duty to exercise oversight of staff and the operations of the association.

In light of recent resignations from Gospel for Asia’s board and the secrecy surrounding current board members, it seems appropriate to consider the duties and responsibilities of board members. In my view, GFA’s board shares responsibility with current leadership for the many questions raised over the past two years. Below are quotes from various authorities on the fiduciary responsibility of nonprofit board members.

Boards of nonprofits are legally responsible for overseeing the organization’s financial management. Since nonprofits receive tax-exempt status by state and federal agencies to fulfill public needs, the board’s obligations go well beyond its organization’s members, constituents, beneficiaries or clients.

An important part of serving the public trust is fulfilling the important stewardship roles of protecting financial and nonfinancial assets, and managing current income properly to fulfill exempt purposes. Although a ministry’s management has the primary responsibility for the organization’s financial management and reporting, the board of directors is ultimately responsible for the process. Outside auditors also play an important role as well. – Dan Busby, Quality Financial Reporting: What is the board’s responsibility?

Speaking of outside auditors, GFA’s auditor Bland Garvey recently resigned according to former board member Gayle Erwin.

GFA’s leaders have maintained an unseemly silence in the face of poor relationships with staff, unaccounted for funds, allegations of mismanagement, and other financial irregularities. The responses from David Carroll and K.P. Yohannan have not been specific and have not addressed certain issues at all. My Calvary Chapel survey results thus far find that former donors and supporting pastors are unsatisfied with the answers given by GFA leaders. At this point, GFA directors have a responsibility to speak to the allegations and transparently disclose what is being done to correct any violations of the public trust. So far, outside of comments from former board member Gayle Erwin, all we have heard is crickets.

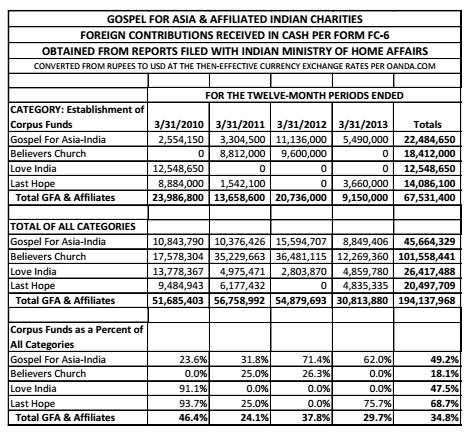

Since GFA is expected to maintain discretion and control over funds sent to Asia, board members need to have knowledge of how those funds are spent and audited. According to Erwin, the GFA board was not given such information. Recently, Erwin told me, “Once the monetary figures went beyond the local, we board members had no knowledge of it. I am embarrassed by how little we knew.” According to Erwin, the board’s information came from K.P. Yohannan and was not contested by other senior leaders who in Erwin’s words, have to do “what K.P. says.”

Because the board of directors is ultimately responsible for the activities of an organization, it can become the target for criticism or legal action when things go wrong, and failure to live up to fiduciary responsibility is a serious charge.

As trustees of the organization’s assets, board members must be able to demonstrate that due diligence has been employed in decision making, particularly with regard to the oversight of financial matters. While individual board members are responsible for their own actions, the full board is responsible for the board’s decisions. This means that board members must hold each other as accountable.

But nothing absolves the board from its single most important responsibility as a fiscally accountable body of trustees – that of acknowledging the responsibilities that come with being a beneficiary of the public trust. Generally speaking, nonprofits are deemed to be holding assets, including investment funds, in trust for the benefit of their constituencies and the charitable purposes for which the organization was formed. Linda Compton, Painful Lesson in Board Investment Policy Making, Boardsource, retrieved from ECFA

Although the primary topic of Compton’s article is about board oversight of retirement funds, the principles that apply to oversight of those funds also apply to all other activities of an organization. Boards can’t merely blame staff when concerns are raised by the public and constituents of the nonprofit. As it is now, GFA lost ECFA membership, is losing donors, and has not resolved the concerns of well over 100 former staff. Three board members have resigned over these issues. The remaining board members have a duty to God and the public to step in and right the ship. Remaining silent doesn’t remove their responsibility.

Although GFA is secretive about their board members, evidence is strong that current board members are K.P. Yohannan (chair), Gisela Punnoose (KP’s wife), Danny Punnoose (his son), Chuck Zink (has a child on staff), Robert Felder, Francis Chan, and David Mains. According to K.P. Yohannan, there is at least one more member but the identity of that member isn’t clear. Looking at the board members, it would take every non-Yohannan family member to take action. One of the requirements to participate in the Combined Federal Campaign is a board made up of independent members. However, it is plain to see GFA does not meet that standard.

Difficult or not, board members have a duty to the public. Christian board members have a duty beyond that. Only time will tell if GFA’s board will rise to the occasion.

Additional resources:

Fiduciary Responsibilities of Nonprofit Directors

A Nonprofit Board’s Fiduciary Responsibility